.jpeg)

From Unemployment to Brexistentialism

The S&P 500 ended the third quarter with a gain of 1.7%. The benchmark US index has weathered growing concerns over slowing US economic data and the still unresolved trade war with China. During the quarter, the Federal Reserve lowered interest rates twice, cutting the government’s overnight lending rate by 50 bps in total. The cuts provided temporary support for equities, but the reality is that fears are mounting over the pressure that the economic conflict with China puts on manufacturing and agricultural industries, as well as the impact for technology companies which have extensive operations in Asia. The combination has investors resetting expectations for valuations and higher risks.

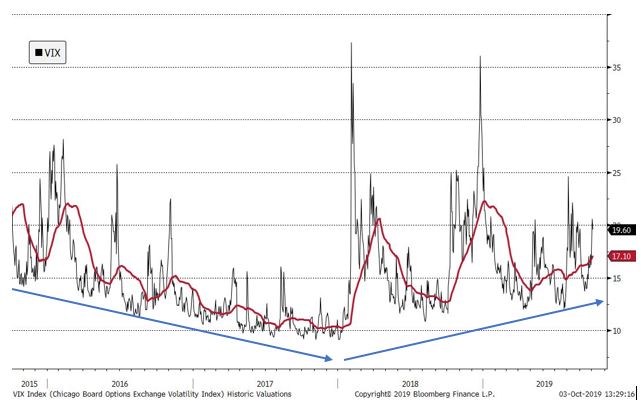

Volatility Rising

Volatility in the equity markets has been steadily rising. After falling for much of the first two years of the Trump presidency, volatility (as measured by the 50-day moving average of the VIX Index) has grown since year-end 2017, even spiking occasionally. As the trade war has escalated (with no real end in sight) and the domestic political landscape has become more antagonistic, the increase in volatility reflects investors’ growing uncertainty of their economic implications.

CBOE VIX Index w/50 day moving average

However, fear is an emotional attribute that we have seen enter and exit the market many times throughout the current 10+ year bull market. So, what would tip the scale and escalate the emotion to tangible reality? Unemployment.

Jobs, Jobs, Jobs

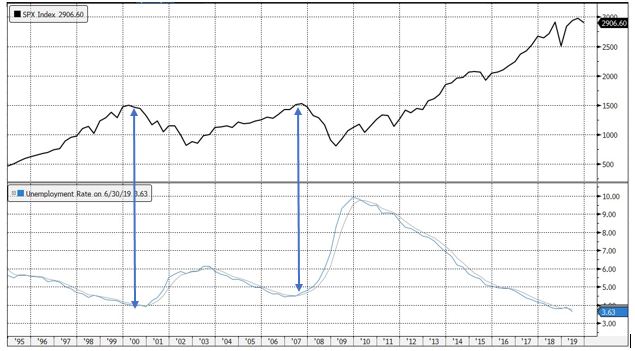

The stock market endures numerous 10%, or even 15%, corrections during the course of typical market cycles. It is therefore helpful to seek confirmatory evidence beyond the actions of equities to gauge when a correction is more than a correction. While numerous confirmatory data series can be selected from the list of leading or coincidental economic indicators, US unemployment statistics are readily available and provide a pretty good warning signal when businesses are indeed reacting to changes in the economy. Additionally, related monthly series can warn of possible changes in the quarterly numbers and it is hard data rather than a “survey”.

We also watch unemployment because it reflects businesses motivations. When companies have a positive outlook they typically don’t downsize. Layoffs and downsizing usually occur when businesses are trying to protect profits and seeking to minimize labor expenses. Admittedly, the indicator works better to flash recession warnings than to predict recoveries, as it takes longer to select and then hire staff than it does to downsize. So when national unemployment ticks up, it is confirmation a significant percentage of the economy has decided to take defensive action to margins and lower expenses.

The chart below shows the 25-year performance of the S&P 500 with the US Unemployment Rate compared to its trend. When the Unemployment Rate breaks trend and begins to tick higher, it has usually marked an economic recession. During the current economic expansion, the US Unemployment Rate has trended firmly lower since the Great Recession of 2008, dropping from 10.7% to 3.5% nationwide. March 2019 saw a slight, inconsequential increase in unemployment before ticking lower again in the second quarter and again this quarter. More interesting, however, is that March was the first quarterly increase in unemployment since June of 2011, or 31 straight quarters.

S&P 500 Index versus US Unemployment w/12-month moving average

So if concerned that market gyrations are the start of the next recession, don’t look at the stock prices, look for material changes in employment trends. Despite a hiccup in March, unemployment is still trending lower.

Chaos Across the Pond

Absent from the US media is the ongoing Brexit saga. We at Oak Associates have been fascinated and perplexed by the Brexit debacle and eagerly anticipate the October 17th deadline to see if UK Prime Minister Boris Johnson is able to reach a deal or if his tactic was to create a No-Deal Brexit, after all. Leaving the EU without a deal would be a catastrophic disaster for the UK economy and yet its Parliamentarians seem unwilling to support a withdrawal agreement and won’t accept No-Deal. Nor can politicians agree on a compromise to a customs union or how to handle the Irish border. Waiting for the EU, who have significantly less at risk than Britain, to blink seems misguided. It is a sort of political Brexistentialism, where the UK seems to believe it can achieve a Brexit miracle by sheer political will. Only time will tell.

Thank you for reading.

Robert Stimpson, CFA

Co-Chief Investment Officer & Portfolio Manager

The investments mentioned or listed in this article may or may not represent an investment currently recommended or owned by Oak Associates for itself, its associated persons or on behalf of clients in the firm’s strategies as of the date shown above. The investments mentioned do not necessarily represent all the investments purchased, sold or recommended to advisory clients during the previous twelve month period. Portfolios in other Oak Associates strategies may hold the same or different investments than those listed or mentioned. This is generally due to varying investment strategies, client imposed restrictions, mandates, substitutions, liquidity requirements and/or legacy holdings, among other things. The particular investments mentioned were not selected for inclusion in this report on the basis of performance. A reader should not assume that investment(s) identified have been or will be profitable in the future.