March 13, 2020

Global and U.S. equity markets continue to endure unprecedented levels of volatility. The Covid-19 pandemic, its potential economic impact, the Administration’s response, and media frenzy are all contributing to substantial market swings and, most significantly, investor uncertainty. The S&P 500 Index has fallen over 20% in the last 17 sessions, essentially ending the 11-year bull market expansion. We continue to urge calm and emphasize rationality over emotionality.

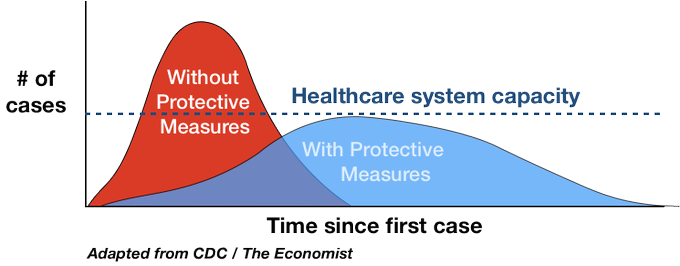

The CDC vs. the Fed

This correction includes characteristics unlike those of past market declines. Historically, the U.S. has experienced minor threats from other flus and viruses but never a global pandemic. This situation is exceptional. In this instance, the Center for Disease Control (CDC) is at the helm rather than the Federal Reserve. The CDC’s plan is straightforward…manage the transmission rate of the virus in an attempt to slow the contagion.

The chart below has recently been utilized by healthcare professionals to explain their endorsement of school closures and the restriction of large public gatherings. Currently, the primary goal of public health officials is to prevent the U.S. healthcare system from being overwhelmed and thus protect the ability to provide core services. By slowing the transmission rate of Covid-19, the total number of infected patients may ultimately be similar, but facilities and resources are less likely to be strained. This is the situation presently occurring in Italy. The byproduct of this plan however is likely to be a prolonged reduction in economic activity.

Recession Risk

Given the changes to personal behaviors and persistent market uncertainty, there is undoubtedly an elevated risk of recession. Oak’s plan of action during market corrections remains the same: stay calm, monitor and evaluate the economic and market environments as they unfold, identify the best investments over the next 3-5 years, and make changes to the portfolio as necessary to capture this opportunity. Our research process already leads us to high-quality companies with sustainable business models and secular growth drivers. We do not believe market timing during downturns is worthwhile. Yet, there is a higher probability that recent events will have a more intermediate-term effect on the economy. This has created attractive relative opportunities that will likely drive incremental changes to the portfolio to better position it to outperform peers in the years to come.

Should we abandon stocks or raise cash?

The recent market correction has been swift and deep. While undeniably painful, sharp declines have historically been followed by higher equity prices 3-, 6- and 12-months out. Extrapolating the recent rout is a common mistake and data confirms that panic selling after a historic decline is the wrong move for long-term investors. Furthermore, stocks continue to offer attractive relative valuations when compared to bonds. The yield on the 10-year US Treasury Notes has fallen to 0.81%. This compares to an earnings yield of 6% on the S&P 500 in addition to a dividend yield of 2.4%. For the long-term investor, the expected return from stocks remains far superior to bonds.

The only consensus is fear.

The sharp decline in US equities has been universal. There have been few safe havens. Apart from gold, all other sectors are down sharply year-to-date and from their February highs. All traditional defensive sectors have suffered, and even non-traditional ones like Bitcoin. This indicates that the selling is widespread and indiscriminate. Safe ports in the storm have been few and far between. Given the likelihood of additional headlines that will rattle the market, more volatility should be expected.

None of this may matter.

We have been through numerous market cycles, extraordinary bear markets, and several financial crises. But no one has been through a global pandemic since the Spanish Flu of 1918. Therefore, it is difficult to know how to proceed or how this pandemic will progress. It is important to admit what you know and what you do not know. What we do know is that stocks recover from extraneous events. Economies recover and global markets rebound. The foundations of our economy are sound and there is no reason to believe that once the pandemic subsides, markets should not recover.

That being said, things have been very chaotic over the past two weeks, and we hope to be clear and concise with clients. This situation is different. We may make changes. Focusing on the long-term is always the best strategy. If you have any questions, please don’t hesitate to call us at 330-668-1234.

Thank you for reading.

Robert Stimpson, CFA, CMT

Co-Chief Investment Officer & Portfolio Manager

Jeff Travis, CFA

Portfolio Manager

The investments mentioned or listed in this article may or may not represent an investment currently recommended or owned by Oak Associates for itself, its associated persons or on behalf of clients in the firm’s strategies as of the date shown above. The investments mentioned do not necessarily represent all the investments purchased, sold or recommended to advisory clients during the previous twelve month period. Portfolios in other Oak Associates strategies may hold the same or different investments than those listed or mentioned. This is generally due to varying investment strategies, client imposed restrictions, mandates, substitutions, liquidity requirements and/or legacy holdings, among other things. The particular investments mentioned were not selected for inclusion in this report on the basis of performance. A reader should not assume that investment(s) identified have been or will be profitable in the future.